Free Supplier Risk Scorecard Download

Download our free supplier risk scorecard here!

Download the free tool!AI Summarize:

Raise your hand if you love financial reporting?

No?

Okay, let's try with a different line.

Do you know how important financial reporting is?

Yes?

Yeah, all business leaders and managers know that.

It's part of running a company, after all. You need to show how accurate and honest your finances are. Not only because it's what the government wants, but because it's also how you demonstrate your reputation across markets, suppliers, and customers alike.

And of course, there are standards to follow. In the U.S, the most common one is the Generally Accepted Accounting Principles, also known as GAAP.

But how can GAAP be applied to AP processes?

It's a question we're going to solve right away.

What's GAAP?

We know what those letters stand for: Generally Accepted Accounting Principles. The definition, though, is a bit broader.

Just like a rulebook filled with guidelines.

But in all seriousness, GAAP comes as the framework for making financial reporting consistent, reliable, and simple to understand.

Created by the FASB (Financial Accounting Standards Board), it works to improve the quality of the financial information you share with your stakeholders.

Another important detail? It's constantly updated, so it never runs out of date.

Is it obligatory?

If you're a publicly traded company, yes; however, following the GAAP might not be a bad idea for private businesses.

You might've to put some extra effort into it, but knowing that your information is accurate and ready for compliance can certainly balance things out.

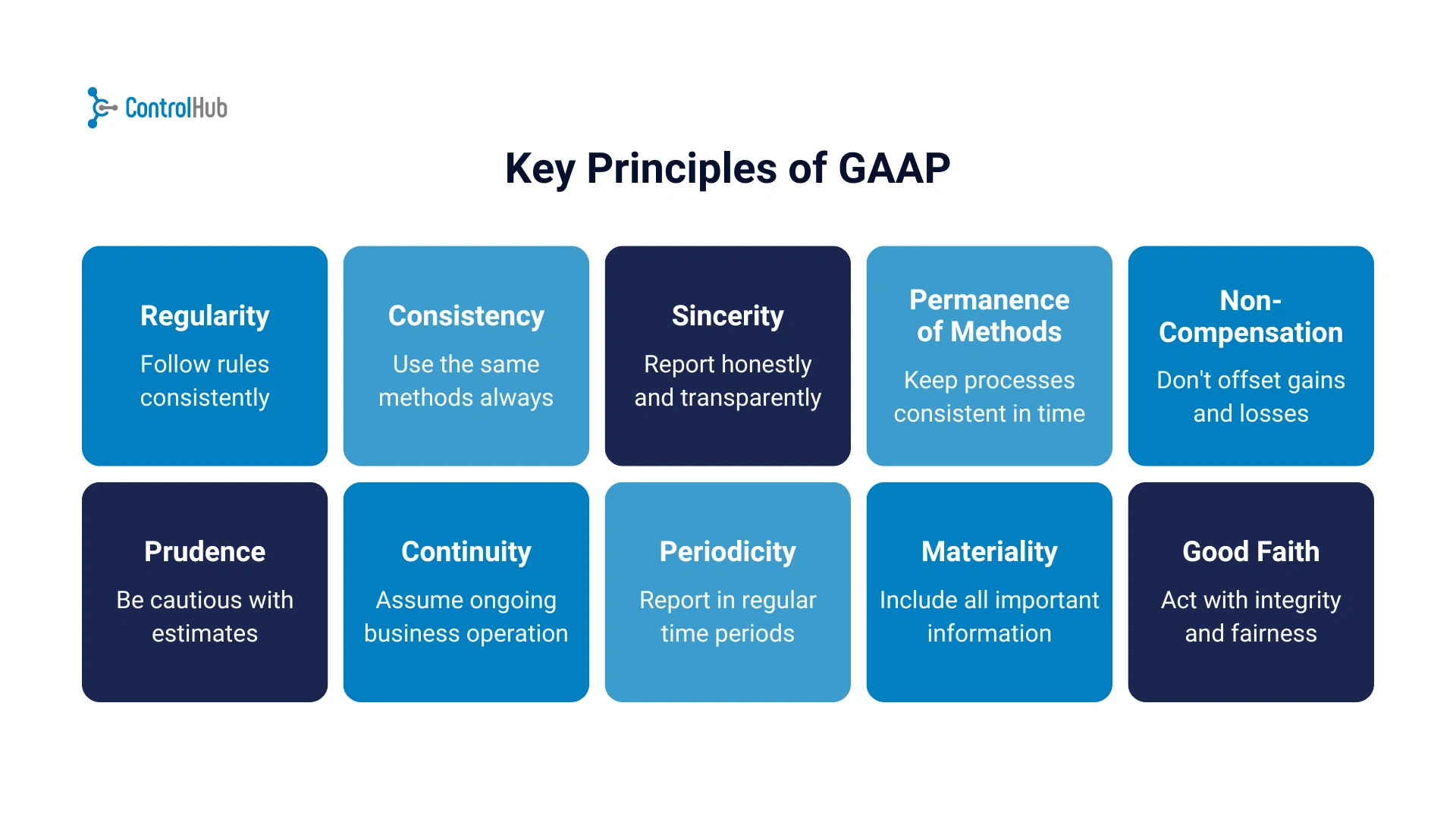

Key Principles of GAAP

We did say that it was like a rulebook, remember?

The best way to actually understand the benefits of implementing GAAP in your AP reporting lies close to knowing what makes GAAP work.

These are the 10 drivers of the GAAP philosophy.

Regularity

You don't just choose to follow a rule whenever you feel like.

It's something you've to do on a daily basis. Every payable must be recorded based on the same standards, no matter what

Consistency

follows up on the first principle.

To really follow GAAP, you need to make sure your staff is sticking with approved accounting methods, which contributes to keeping your AP data standardized.

Sincerity

One thing about GAAP?

Values are absolutely important.

And being honest is at the top of the list.

You don't want to make something look better than what it actually is in reality.

Permanence of methods

Use the same systems and processes over time. If you’ve been categorizing trade payables one way, don’t switch it up without documentation and explanation.

Non compensation

Don't try to add unnecessary details or remove pieces of information just because you think it'd be better that way. If you owe a huge quantity of money to a supplier, record it as it is.

Prudence

Do you know a liability is coming your way?

If there’s a chance you’ll owe money, record it. Don’t wait for a payment dispute to be resolved before acknowledging the payable.

Continuity

This principle assumes your business is a going concern, that it’ll keep operating. It affects how you value and report liabilities over time.e

Periodicity

Do you know how finances work around certain specific periods of time?

This principle is all about that. Financial reports are broken into time periods like months or quarters.

Materiality

The weight is on the impact

If a payable is so insignificant that it won't have any impact on your decisions, it doesn't need the same level of attention as larger transactions.

Good faith

The most important

Act with honesty and complete integrity.

Free Supplier Risk Scorecard Download

Download our free supplier risk scorecard here!

Download the free tool!How is GAAP Used for Accounts Payable?

Okay, so the principles are practically a group of morals to be followed.

But how can you use those values to the benefit of your AP?

Accrual-based accounting

This is probably a method you're already familiar with. Following an accrual-based approach means you record the expenses the moment they happen and not when payment is due. So, let's say, you receive your order in the middle of the month, that's when the liability goes into the books, even when you don't have to pay for it until the next month.

Proper classification

Remember that Accounts Payable is a liability, it should be registered as such yes, but it also needs to be recorded as AP so it's separated from other types of responsibilities.

While it seems like an obvious one, doing this guarantees that when someone comes and goes over your company's financial situation, they get the right picture.

Timely and accurate recognition

This follows the idea of using an accrual-based method for your liabilities. GAAP prefers you to recognize that financial obligation as soon as they incur, so if you receive an invoice, you know it's time to register it

Financial statement disclosures

GAAP requires companies to be completely transparent about the balances of their AP in their financial statements.

It's a good practice to keep a visual representation of your financial obligations, a practice that facilitates any related decisions you have to make at some point, like maybe asking for a loan or entering into a new market.

Methodology

You won't believe how following a single methodology can simplify things.

Especially if financial reports are in between.

As we've learnt in the principles section, GAAP promotes the idea of always adhering to the same approach, so if you're doing your AP processes one way this quarter, you must keep the approach the next one.

Materiality

Not every small payable needs intense scrutiny. If it’s not likely to impact financial decisions, you have some flexibility in how you treat it. That said, material payables should always be recorded accurately and disclosed when relevant.

Free Supplier Risk Scorecard Download

Download our free supplier risk scorecard here!

Download the free tool!The Importance of Internal Controls for GAAP and AP

Accounts payable have a reputation for being a complicated matter.

Unless you make sure everything is accounted for.

The simplest approach to achieve it?

Work with internal controls

From a GAAP perspective, internal controls play a big role in establishing accuracy and consistency.

Since GAAP requires expenses to be recorded in the right period and matched with the right activities, internal controls help support that. For example, making sure your supplier invoices are logged on time and reviewed before payment is a positive step in guaranteeing your liabilities are complete and correctly reported.

They also help prevent mistakes, both accidental and intentional…which aren't mistakes at all.

Simple steps like requiring dual approvals for payments or flagging duplicate invoices can go a long way in reducing risk for your whole business.

Differences between GAAP and IFRS

Before we go, let's make a quick revision between GAAP and IFRS.

The IFRS, which, by the way, stands for International Financial Reporting Standards, is pretty similar to what we've seen so far with GAAP. It also works to bring consistency and transparency to financial reporting, but it does it in a slightly different way.

Less rigid, if you will

Here are some key differences between GAAP and IFRS:

Geography

GAAP is used primarily in the United States.

IFRS is the global standard, used in over 140 countries.

So if you're doing business abroad, it's about time to get familiar with how IFRS works.

Principles vs. rules

GAAP is ideal for those who love to play by the rules, which means it lays out detailed guidelines for handling specific situations.

IFRS offers broader guidelines that require more judgment in application.

Flexibility

GAAP is considered to be rigid due to its detailed rules.

IFRS allows a bit more flexibility and interpretation, especially in areas like classification and recognition.

Accounts Payable

In general, AP is classified similarly under both frameworks, as a current liability.

However, timing and recognition can vary slightly, especially when it comes to estimates or judgment-based entries.

Inventory accounting

GAAP allows LIFO (Last In, First Out) for inventory costing, IFRS does not.

While not directly AP-related, this can affect COGS and impact your supplier's payment strategies.

Financial statement presentation

IFRS provides fewer line-item requirements and often gives you higher liberty in the way you format statements.

GAAP is as serious as it gets, coming with prescriptive formats and disclosure requirements.

Disclosure requirements

GAAP works better around detailed disclosures, particularly around liabilities and contingencies.

IFRS focuses on the substance over the form of transactions and may give you room for summarization.

Free Supplier Risk Scorecard Download

Download our free supplier risk scorecard here!

Download the free tool!Free Supplier Risk Scorecard Download

Download our free supplier risk scorecard here!

Download the free tool!Key Takeaways

- GAAP provides the structure for how accounts payable should be recorded, reported, and disclosed, ensuring your financials are consistent and trustworthy.

- Accrual accounting is central to GAAP, meaning you record expenses when they’re incurred, not when they’re paid.

- Classification matters, AP is a current liability, and it needs to be presented clearly on your balance sheet under GAAP rules.

- Internal controls play a critical role in supporting GAAP compliance by preventing errors, reducing fraud risk, and keeping your AP process audit-ready.

- GAAP vs. IFRS: While both aim to standardize financial reporting, GAAP is more rules-based (common in the U.S.), while IFRS is principles-based and used internationally.

%20(1).avif)

.png)